The new operating system of sustainable finance

Let me start with a few observations about the financial markets:

- More than one million companies in Europe are expected to prepare data according to sustainability reporting standards. That is a large number and expect the trickle-down effect to be real.

- On average, the cost of capital is lower for companies with a good ESG profile.

- Financial intermediaries need to give capital owners relatively detailed information about the non-financial characteristics of their portfolio companies. They can also charge higher fees for sustainability-related products.

- While regulators seek to redirect capital flows toward sustainable initiatives, many market participants remain focused on compliance checklists, often missing the full picture.

It could be straight out of Greek mythology. A lot of chaos and confusion.

The efficiency of traditional financial markets

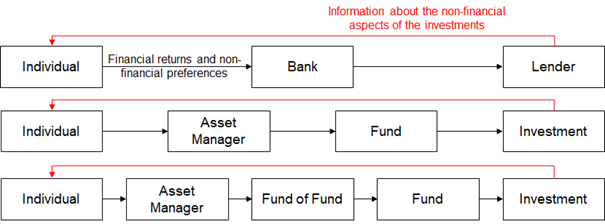

The financial markets tend to be intermediated. That means that there are always institutions between the capital owners which supply capital and companies that require capital. An individual only rarely invests directly into companies.

This value chain of capital can consist of a single bank or different asset managers and funds which allocate capital.

The traditional system is noteworthy in two regards:

- It is only managed by optimizing risk-return profiles. If an insurance company selects a fund of fund, it happens only on the expected risk-adjusted financial returns.

- The information flow tends to happen between only the two instances next to each other. The bank will only provide basic information but will not provide detailed information about the lenders.

This works surprisingly efficiently as every intermediary is selected to maximize financial returns, while minimizing risks.

The new paradigm

The new global regulatory sustainability-focused landscape for the financial markets is built around two levers which are to (1) change the economics of companies and to (2) redirect capital flows.

The economics of companies have been impacted by actions plans such as the Green Deal in the European Union or elements of the Inflation Reduction Act in the US. These policy measures make Greenhouse Gas Emissions more expensive, provide subsidies for renewable energy or make capital cheaper for investments in those areas. These measures are remarkably successful in achieving its objectives.

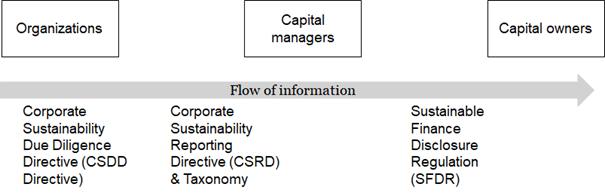

The financial regulation is focusing on the disclosure of relevant information and thereby influencing the investment processes of capital owners.

The illustration below shows how the two levers are impacting the economics of companies as well as those of financial intermediaries.

Financial regulation

The financial regulation is based on the understanding that only the financial institutions, respectively the capital owners decide where to allocate capital. For example, the accompanying documents for the EU policies clearly state the aim of the regulation is to improve the flow of capital by enabling investors to have a complete picture of the risks and opportunities. This requires two steps:

- Financial intermediaries need to process and provide this information to capital owners (and implement adequate risk management systems)

- Companies need to provide information on their non-financial performance

In Europe, the following directives and regulations structure the flow of information to the capital owners.

It is not as clearly structured in the United States, but the SEC has proposed rules on climate disclosure and issued guidance on ESG funds. In addition, there are voluntary standards for green bonds or ESG reporting. We can expect a certain degree of convergence for the global standards.

Investment decisions

Institutional investors were usually avoiding impact investments as their risk-return profiles are less attractive. While a normal mezzanine fund may offer returns of approximately 10–15%, a typical impact investment loan fund would offer returns in the range of 5%.

However, the regulatory changes as well as pressure from stakeholders, divestment activists and capital owners mean that financial intermediaries need to integrate non-financial criteria in their investment decision. Check out this delightful book on how university endowment managers need to consider all kind of non-financial preferences from their stakeholders and the trade-offs.

There is already a large body of research showing how non-financial criteria are integrated in financial decision-making processes and valuations. For example, research shows that the implied cost of capital for green companies is lower than for non-green companies. In addition, financial intermediaries start to take their ownership responsibility more seriously and take decisions when it comes to compensation or long-term strategies.

The underlying IT solutions

Applying a computer science perspective gives us a large set of distributed, decentralized and largely independent actors (companies) which require funding from another set of distributed, decentralized and largely independent actors (financial intermediaries). Traditionally, the investment decisions were taken based on financial returns and recommendations from research analysts.

However, a growing share of the information flow is starting to be exchanged using a semantic layer. This sematic layer requires a set of IT solutions which take advantage of advances in natural language processing and knowledge graphs as much of the underlying data is written text.

We are also facing the situation that the information has to flow from the lender or the investment back to the individual capital owners. This is not straightforward and requires steps to aggregate the data from various sources.